Tax season can be a stressful time for many, but it’s also an opportunity to maximize your financial benefits. Understanding tax deductions and credits is crucial for keeping more money in your pocket. Let’s explore how you can make the most of these often-overlooked opportunities to reduce your tax burden and potentially increase your refund.

Understanding the Difference Between Deductions and Credits

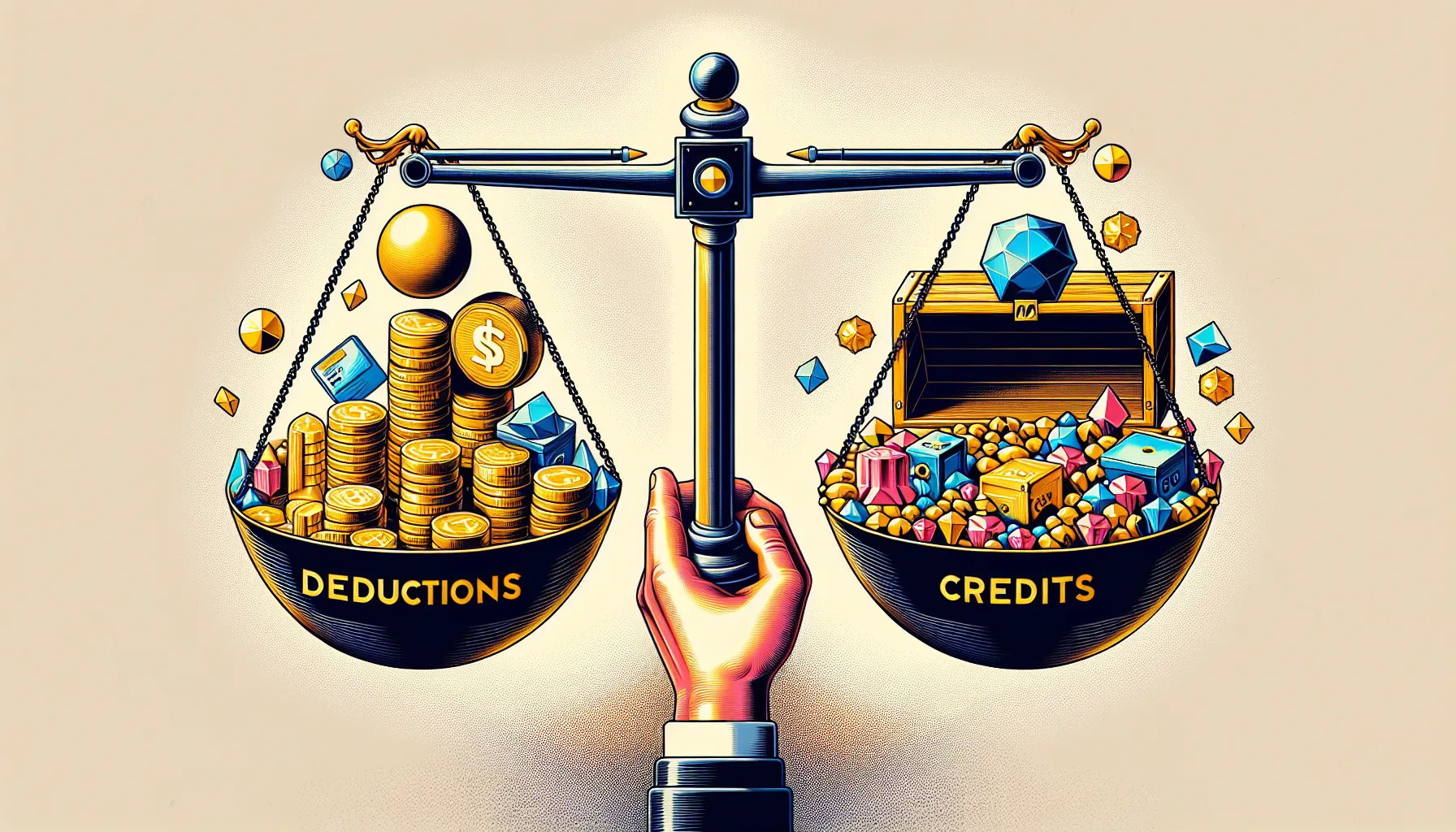

Before diving into specific tax-saving strategies, it’s important to understand the fundamental difference between tax deductions and tax credits. Tax deductions reduce your taxable income, while tax credits directly reduce the amount of tax you owe. Both can significantly impact your final tax bill, but they work in different ways.

Tax deductions are subtracted from your gross income before your tax is calculated. This means they lower your taxable income, which can potentially put you in a lower tax bracket. For example, if you earn $50,000 and claim $10,000 in deductions, you’ll only be taxed on $40,000 of income.

Tax credits, on the other hand, are applied after your tax is calculated. They provide a dollar-for-dollar reduction of your tax liability. For instance, if you owe $3,000 in taxes and qualify for a $1,000 tax credit, your tax bill would be reduced to $2,000. This makes tax credits generally more valuable than deductions of the same amount.

Common Tax Deductions You Might Be Missing

Many taxpayers overlook valuable deductions that could significantly reduce their taxable income. Here are some common deductions you should be aware of:

Charitable donations are a frequently overlooked deduction. Keep records of all your charitable contributions, including cash donations and the fair market value of donated goods. Even small donations can add up over the year and make a difference on your tax return.

If you’re a homeowner, you may be able to deduct mortgage interest and property taxes. These deductions can be substantial, especially in the early years of your mortgage when a larger portion of your payment goes toward interest. Don’t forget to include any points paid on your mortgage as well.

For those who are self-employed or work from home, home office deductions can provide significant tax savings. You can deduct a portion of your rent or mortgage, utilities, and maintenance costs based on the percentage of your home used exclusively for business purposes. However, be sure to follow IRS guidelines carefully to avoid triggering an audit.

Medical expenses that exceed 7.5% of your adjusted gross income can also be deducted. This includes costs for doctors, dentists, hospitals, prescription medications, and even travel expenses related to medical care. Keep detailed records of all your medical expenses throughout the year to take full advantage of this deduction.

Maximizing Your Tax Credits

Tax credits can have an even more significant impact on your tax bill than deductions. Here are some valuable credits you shouldn’t overlook:

The Earned Income Tax Credit (EITC) is designed to benefit low to moderate-income workers. The amount of the credit varies based on your income, filing status, and number of children. Many eligible taxpayers fail to claim this credit, potentially missing out on thousands of dollars.

If you have children, the Child Tax Credit can provide substantial savings. As of 2021, this credit is worth up to $3,000 per child aged 6-17 and $3,600 for children under 6. Even if you don’t owe taxes, you may be eligible to receive this credit as a refund.

For those pursuing higher education, the American Opportunity Credit and the Lifetime Learning Credit can help offset the costs of tuition and related expenses. The American Opportunity Credit is worth up to $2,500 per eligible student, while the Lifetime Learning Credit can provide up to $2,000 per tax return.

Homeowners and renters looking to make their living spaces more energy-efficient should consider the Residential Renewable Energy Tax Credit. This credit applies to solar panels, wind turbines, and geothermal heat pumps installed in your home, potentially saving you thousands on your tax bill while also reducing your energy costs.

Keeping Accurate Records for Tax Time

To take full advantage of tax deductions and credits, maintaining accurate records throughout the year is crucial. Create a system for organizing receipts, bills, and other financial documents. This will not only make tax preparation easier but also ensure you don’t miss out on any potential savings.

Consider using a digital app or software to track your expenses. Many of these tools can categorize your spending automatically, making it easier to identify potential deductions. If you’re self-employed or have a side hustle, keeping business and personal expenses separate is essential. You might want to read about the importance of separating business and personal finances for more insights.

Don’t forget to keep records of any job-hunting expenses, educational costs related to your current job, and unreimbursed employee expenses. While some of these deductions have been limited by recent tax law changes, they may still apply in certain situations.

Seeking Professional Help

While understanding tax deductions and credits is important, tax laws can be complex and change frequently. Consider consulting with a tax professional or certified public accountant to ensure you’re taking advantage of all available tax benefits. They can provide personalized advice based on your specific financial situation and help you develop a long-term tax strategy.

If you’re a small business owner or self-employed, professional help can be particularly valuable. A tax expert can guide you through the intricacies of tax strategies for small business owners, potentially saving you significant amounts of money.

Remember, the cost of professional tax preparation may itself be tax-deductible, making it a worthwhile investment in your financial future.

Planning Ahead for Next Year’s Taxes

Tax planning shouldn’t be a once-a-year activity. By thinking about taxes year-round, you can make strategic decisions that maximize your deductions and credits. Consider adjusting your withholdings if you consistently receive large refunds or owe significant amounts. This can help you better manage your cash flow throughout the year.

If you’re nearing retirement, it’s crucial to understand how your tax situation may change. Retirement planning in the age of longevity can help you prepare for potential changes in your tax obligations and opportunities for tax savings in your golden years.

By staying informed about tax deductions and credits and planning ahead, you can ensure you’re not missing out on valuable opportunities to keep more of your hard-earned money. Remember, every dollar saved on taxes is a dollar that can be put towards your financial goals, whether that’s building an emergency fund, investing for the future, or enjoying life’s pleasures.

Frequently Asked Questions

What’s the difference between tax deductions and tax credits?

Tax deductions reduce your taxable income before tax is calculated, while tax credits directly reduce the amount of tax you owe after it’s calculated. Credits generally provide more savings dollar-for-dollar compared to deductions of the same amount.

What are some commonly overlooked tax deductions?

Commonly overlooked tax deductions include charitable donations, mortgage interest and property taxes for homeowners, home office expenses for self-employed individuals, and medical expenses exceeding 7.5% of adjusted gross income.

How can I maximize my tax credits?

To maximize tax credits, consider claiming the Earned Income Tax Credit (EITC) if eligible, utilize the Child Tax Credit if you have children, and explore education-related credits like the American Opportunity Credit or Lifetime Learning Credit if pursuing higher education.

Why is record-keeping important for tax purposes?

Accurate record-keeping is crucial for taking full advantage of tax deductions and credits. It helps you track potential deductions, makes tax preparation easier, and ensures you don’t miss out on any savings. Consider using digital apps or software to organize financial documents.

Should I seek professional help for my taxes?

Consulting with a tax professional or certified public accountant can be beneficial, especially if you have a complex financial situation or are self-employed. They can provide personalized advice, help you navigate complex tax laws, and potentially save you money in the long run.