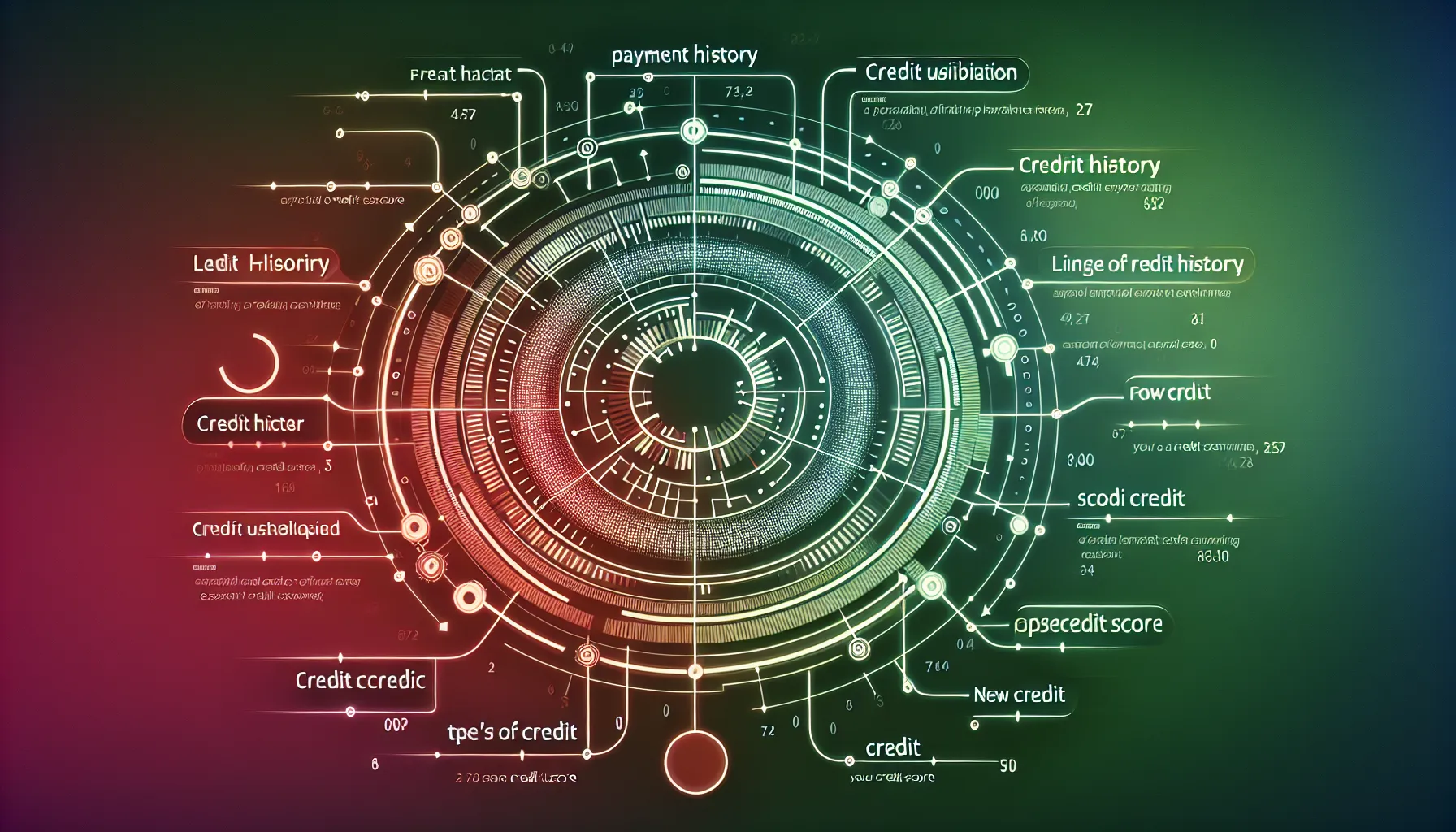

Your credit score is a vital component of your financial health, influencing everything from loan approvals to interest rates. Understanding the factors that impact your credit score can help you make informed decisions and improve your financial standing. Let’s explore the key elements that shape your credit profile.

Payment History: The Cornerstone of Credit

Your payment history is the most significant factor affecting your credit score, accounting for about 35% of the calculation. Lenders want to see how reliably you’ve repaid past debts, as this indicates how likely you are to repay future loans.

Consistently making on-time payments is crucial for maintaining a good credit score. Late payments, especially those more than 30 days overdue, can significantly harm your credit. The impact of late payments lessens over time, but they can remain on your credit report for up to seven years.

If you’re struggling to make payments, it’s better to communicate with your creditors rather than miss a payment. Many lenders offer hardship programs or payment plans that can help you stay on track without damaging your credit score.

Credit Utilization: Balancing Your Debt

Credit utilization refers to the amount of credit you’re using compared to your credit limits. This factor accounts for about 30% of your credit score. Generally, it’s recommended to keep your credit utilization below 30% of your available credit.

For example, if you have a credit card with a $10,000 limit, try to keep your balance below $3,000. High credit utilization can signal financial stress to lenders and negatively impact your score.

To improve this aspect of your credit, consider paying down your balances and avoiding maxing out your credit cards. If you consistently approach your credit limits, you might want to request a credit limit increase or create a budget to manage your spending.

Length of Credit History: The Value of Time

The length of your credit history makes up about 15% of your credit score. This factor considers how long you’ve had credit accounts and the average age of all your accounts.

A longer credit history provides more data for lenders to assess your creditworthiness. It’s generally beneficial to keep old credit accounts open, even if you’re not using them frequently. Closing old accounts can shorten your credit history and potentially lower your score.

If you’re new to credit, don’t worry. While you can’t instantly create a long credit history, you can start building good credit habits now. Consider becoming an authorized user on a family member’s long-standing credit card or opening a secured credit card to begin establishing your credit history.

Credit Mix: Diversifying Your Credit Portfolio

Your credit mix accounts for about 10% of your credit score. Lenders like to see that you can responsibly manage different types of credit, such as revolving credit (like credit cards) and installment loans (like mortgages or car loans).

Having a diverse credit mix shows that you’re a well-rounded borrower. However, this doesn’t mean you should open new credit accounts just for the sake of diversity. Only apply for and use credit that you actually need.

If you’re looking to diversify your credit mix, consider options that align with your financial goals. For instance, if you’re planning to buy a home, learning about mortgages can help you prepare for this significant credit event.

New Credit Inquiries: The Impact of Credit Applications

New credit inquiries make up about 10% of your credit score. When you apply for new credit, lenders perform a hard inquiry on your credit report. Too many hard inquiries in a short period can lower your credit score, as it may indicate financial distress.

It’s important to be strategic about when and how often you apply for new credit. If you’re rate shopping for a specific loan, like a mortgage or auto loan, multiple inquiries within a short timeframe (usually 14-45 days) are typically counted as a single inquiry.

Before applying for new credit, consider whether you really need it and if you’re likely to be approved. You can use soft inquiries, which don’t affect your credit score, to check your own credit or get pre-qualified offers.

Additional Factors: The Complete Picture

While the factors mentioned above are the primary drivers of your credit score, other elements can also play a role. These may include:

- Public records: Bankruptcies, foreclosures, or civil judgments can severely impact your credit score.

- Address changes: Frequent moves might be seen as a sign of instability.

- Employment history: While not directly factored into your credit score, stable employment can be viewed favorably by lenders.

It’s also worth noting that credit scoring models may vary slightly between different credit bureaus. That’s why it’s important to regularly review your credit reports from all three major bureaus: Equifax, Experian, and TransUnion.

Conclusion: Taking Control of Your Credit

Understanding the factors that affect your credit score empowers you to take control of your financial future. By focusing on making timely payments, managing your credit utilization, maintaining a long credit history, diversifying your credit mix, and being cautious with new credit applications, you can work towards improving and maintaining a healthy credit score.

Remember, building good credit takes time and consistent effort. If you’re looking to improve your credit score, check out our guide on strategies for improving your credit score. With patience and good financial habits, you can achieve a strong credit profile that opens doors to better financial opportunities.

Frequently Asked Questions

What is the most important factor affecting my credit score?

Payment history is the most significant factor, accounting for about 35% of your credit score calculation. Consistently making on-time payments is crucial for maintaining a good credit score.

How much of my available credit should I use?

It’s generally recommended to keep your credit utilization below 30% of your available credit. For example, if you have a credit card with a $10,000 limit, try to keep your balance below $3,000.

Does closing old credit accounts improve my credit score?

No, closing old credit accounts can potentially lower your score by shortening your credit history. It’s generally beneficial to keep old credit accounts open, even if you’re not using them frequently.

How do new credit applications affect my credit score?

New credit inquiries make up about 10% of your credit score. Too many hard inquiries in a short period can lower your score, as it may indicate financial distress. Be strategic about when and how often you apply for new credit.

Can I check my own credit score without affecting it?

Yes, you can use soft inquiries to check your own credit or get pre-qualified offers without affecting your credit score. These soft inquiries don’t impact your credit score like hard inquiries do.